Just after the market closed yesterday there was a certain amount of press regarding a move by Fitch Ratings to downgrade the preferred stocks issued by a couple dozen U.S. Real Estate Investment Trust (REIT) companies.

As a researcher, I am always focused on one primary question – what does it really mean for preferred stock investors? So this move by Fitch caught my attention.

More precisely, Fitch modified its formula for rating REIT-issued preferred stocks and that modification resulted in a variety of downgrades. Although some of the headlines made this sound alarming (which, of course, is the purpose of headlines), there was something about the listed companies that just seemed odd.

Fitch, and those reporting this story yesterday, forgot to mention that the majority of the affected companies do not have any preferred stocks that are currently actively trading.Of the 21 affected REITs, only eight have preferred stock issues that are currently actively traded and only two of these companies have more than one such issue.

For the remaining 13 companies, this move by Fitch was merely an academic exercise; one that those reporting on the move should have made clear.

And then there is the other question: do the holders of the affected preferred stocks really care what Fitch thinks?

One way to answer that question is to look at how The Market reacted today, the day after Fitch’s big announcement.

Judging what The Market thinks about anything is tricky business to begin with. Prices have been falling for the last three days in reaction to the Obama plan to levy special taxes on banks.

But if The Market cared about the Fitch downgrades I would expect that the market price of the preferred stock issues that Fitch downgraded below investment grade would fall more than the issues that, even though they were downgraded, remained in investment grade territory.

Here’s today's market reaction to the Fitch preferred stock downgrades: the market price of the issues that were downgraded below investment grade fell an average of $0.10 while the issues that were downgraded, but remained in the investment grade category, fell an average of $0.44. This is the exact opposite result that we would expect if The Market was going to react to Fitch.If The Market had any kind of reaction to the Fitch preferred stock downgrades you sure cannot tell by how holders traded their shares today. Now I realize that the sample size here is pretty slim to draw any big conclusions from; but that’s my point too. Fitch’s new preferred stock rating method does not really apply to anything.

If you’ve read my book, Preferred Stock Investing, you know that I follow the ratings issued by Moody’s more so than their competitors (Standard & Poor’s and Fitch). Subscribers to the CDx3 Notification Service are provided with real-time links to the preferred stock ratings by Moody’s.

Pre-credit crisis, it made little difference as the ratings from these three companies were extremely consistent. But by their own admission, the models used by these rating companies did not anticipate or accommodate the massive and simultaneous devaluation of U.S. real estate and everything connected to it.

The resulting litigation will continue for many more years and these agencies have been stumbling all over themselves ever since to show who can issue more downgrades. S&P changed its bank rating formulation last summer such that it would result in more downgrades, then Moody’s did the same thing last November. Now we see Fitch going after real estate companies.

But since Fitch’s efforts seem focused on companies that really do not have any currently actively traded preferred stocks their motivation for doing this becomes less clear than it should be.

If Fitch is feeling the need to re-establish some credibility, they appear to have missed an opportunity yesterday.

Many Happy Returns.

Friday, January 22, 2010

Fitch Goes After REIT Preferred Stocks But Does Anybody Care?

Monday, January 18, 2010

Building Your Own Preferred Stock Portfolio - How Much Better Is It?

As investors we make judgments about our investment choices continually. Preferred stock investors generally favor lower-risk alternatives since they invest primarily for the reliable periodic dividend income that preferreds can provide.

But many preferred stock investors are left wondering whether they are better off by (A) building their own portfolio of specific preferred stock issues or (B) investing in a preferred stock fund (such as the iShares Exchange Traded Fund PFF).

PFF is composed primarily of preferred stocks issued by banks (90%) or biased toward issues rated below investment grade (30%). Low-rated preferreds issued by banks are precisely the types of preferreds that risk-adverse preferred stock investors have viewed as lower quality investments since the Global Credit Crisis began in June 2007.

While investing in a fund is more convenient, is it enough so to give up the benefits of building your own preferred stock portfolio?

By building your own portfolio you can pick and choose the highest quality issues, but you’ll have to figure out which ones to buy and do so over a longer period of time.

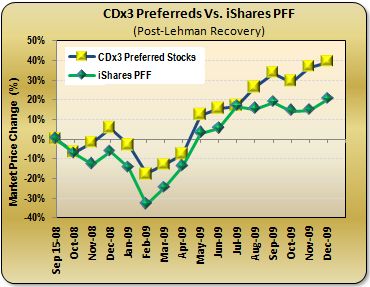

I took a look at these two alternative approaches to preferred stock investing since the Lehman Brothers collapse on September 15, 2008. Since that watershed event, the market has seen both extreme downward and extreme upward movement so I thought it would provide an interesting study period.

I define high quality preferred stocks (“CDx3 Preferred Stocks”) as those that meet the ten selection criteria from my book, Preferred Stock Investing (e.g. rated investment grade, issued by a company that has never suspended dividends, have cumulative dividends and have yet to reach their call date). This chart compares the price performance of these two very different preferred stock investing strategies (building your own portfolio of high quality preferred stocks versus investing in shares of the iShares PFF fund) since the Lehman collapse on September 15, 2008.

This chart compares the price performance of these two very different preferred stock investing strategies (building your own portfolio of high quality preferred stocks versus investing in shares of the iShares PFF fund) since the Lehman collapse on September 15, 2008.

Higher quality preferred stocks fell far less than poorer quality issues at the bottom (-17% compared to -33%) and have gained much more ground since then (+40% compared to +20%). That’s about half the downside and twice the upside by building your own portfolio of the highest quality preferred stocks.

But what about the time it takes to find just the highest quality preferred stock issues out of the 1,000 to 2,000 that are trading every day? My book, Preferred Stock Investing, explains how to screen, buy and sell the highest quality preferred stocks. All of the websites and other resources needed to do so are included.

But for those who would rather someone else do the research and calculations, I offer the CDx3 Notification Service. We do the research, you make the decisions.

Many Happy Returns.

Thursday, January 7, 2010

S&P Report Documents (again) Why It’s Great To Be A Preferred Stock Investor

Standard & Poor’s has just reported the common stock dividend results for 2009 and it is very sobering. There are a number of reasons why people invest in preferred stocks, rather than common stocks, and S&P’s report reminds us of why it’s great to be a preferred stock investor (once again).

Companies issue two kinds of stock – (1) common stock and (2) preferred stock.

Whether or not a share of common stock pays you a dividend is up to the company’s board of directors and they review whether or not to do so every three months.

My research is focused on the highest quality preferred stocks – those that can meet the ten selection criteria found in chapter 7 of my book, Preferred Stock Investing. Two of the criteria that a regular preferred stock must meet are (1) that the dividend be for a fixed amount (usually well above that paid by the same company’s common stock) and cannot be changed by the board of directors or anyone else and (2) the dividend payments must be “cumulative” (meaning that in the odd event that the issuing company misses a dividend payment to you they have to make it up later; they still owe you the money).

Because of these differences (and several others) investors seeking lower risk are often more attracted to preferred, rather than common, stock investing.

Looking over the results of the 2009 common stock dividend performance from S&P makes it pretty clear why preferred stock investors have made the right call once again.

While the highest quality preferred stocks paid an average annual dividend return of 9.61% for 2009 (not to mention an average 97% capital gain on investor principal), Standard & Poor’s reported (click to see article) on Thursday that in 2009:

* the most common stock dividend cuts, and the fewest common stock dividend increases, since S&P started collecting this data in 1955; and

* the common stock dividend cuts cost investors $58 billion in lost dividend income.

Those investing in the highest quality preferred stocks throughout 2009 are not only now earning north of 9% in fixed dividend returns on their money, 100% of the dividends were paid on time and in full. There were no cancelations or cuts whatsoever; quite the opposite.

There are times in one’s life where taking tons of risk for a shot at the big bonanza can be very appealing. If you are in that boat, great. Knock yourself out.

But as America’s population ages, and more investors are less in a position to take risks with money they are counting on, the types of results offered by the highest quality preferred stocks, when compared to common stocks, are consistently compelling, year after year. 2009 was no exception.

Many Happy Returns.